China-focused stablecoin data, retail investor participation and skeptical BTC derivatives markets are all signs that Bitcoin price is not primed for a new all-time high.

Bitcoin closed at its highest level in two months on Sept. 28 and is currently approaching the $66,000 mark. This movement followed gains in the S&P 500 index, which reached an all-time high on Sept. 26, fueled by robust economic indicators and measures aimed at boosting markets and investor confidence in China. However, several metrics indicate that Bitcoin is far from entering a bull market.

Bitcoin/USD (right) vs. S&P 500 futures (left). Source: TradingView

Investor skepticism clouds Bitcoin’s recent rally

Investors could be skeptical due to previous rejections at $70,000 or fearing that a potential recession is underway, which would negatively impact risk-on markets, including cryptocurrencies.

Although this sentiment does not guarantee a sell-off, it makes it easier for bears to instill fear, uncertainty, and doubt (FUD) to suppress Bitcoin’s price. Regardless of what is dampening Bitcoin traders’ spirits, there is no guarantee that its price will continue to benefit from the stock market’s bullish momentum.

Some analysts argue that central banks’ shift to expansionist monetary policy indicates that economies are at risk. Contrary to common belief, this does not necessarily imply high odds of a market bubble bursting, as mega-cap tech companies are able to capture value even in times of declining revenues.

With high margins and strong balance sheets, companies like Google, Amazon, Apple, and Microsoft can benefit from discounted niche acquisitions and face less competition for new hires and equipment, including microchips for artificial intelligence use. In fact, an overheated economy is a net negative for margins, as it creates shortages and high logistics fees.

Meanwhile, for Bitcoin, investors might still value its scarcity and sovereignty, but its drivers significantly diverge from those of the traditional stock market. Moreover, historically, when investors fear a looming recession, they tend to seek shelter in gold, short-term government bonds, and companies that dominate their field.

In essence, even if the S&P 500 continues to make new highs, that does not necessarily mean Bitcoin’s price will benefit. Therefore, Bitcoin bulls need to analyze whether the underlying conditions have changed since the multiple rejections at $70,000 before concluding that lower interest rates and higher government debt are enough to push BTC’s price higher.

For starters, the Coinbase exchange mobile app ranked number 385 on Sept. 28, according to user COINAppRankBot on the X social network. While this represents an improvement from position 482 on Sept. 14, it indicates a lackluster retail investor appetite even as Bitcoin’s price gained 21% in three weeks. Yet a Bitcoin bull could argue the glass is “half full,” as there is still room for improvement.

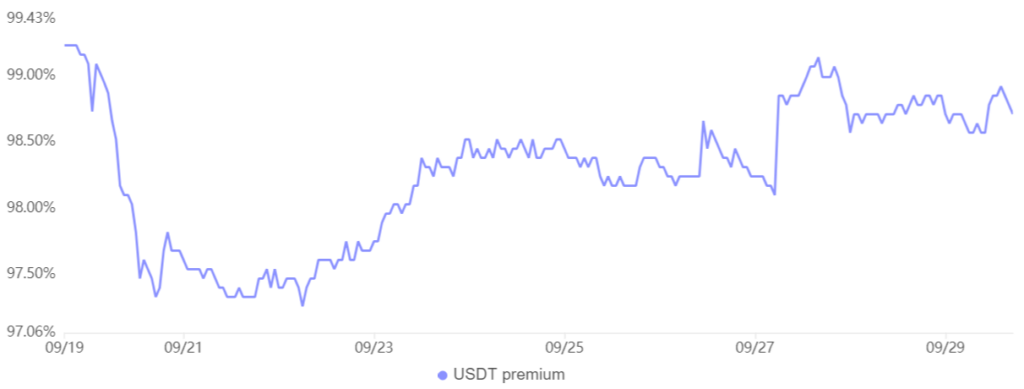

China’s stablecoin discount signals bearish sentiment amid institutional inflows

Inflows from institutional investors might have driven the recent surge in Bitcoin’s price, and data from spot exchange-traded funds (ETFs) corroborate this thesis. However, recent data from Chinese markets show the opposite trend. By examining the demand for stablecoins in China, we can gauge whether investors are entering or exiting the cryptocurrency markets.

Typically, excessive demand causes stablecoins to trade at a premium of 1.5% or higher compared to the official US dollar rate, whereas bear markets result in a discount.

USD Tether (USDT) peer-to-peer trades vs. USD/CNY. Source: OKX

The USDT premium in China has remained below parity for the past two weeks, indicating bearish sentiment. This metric contradicts the recent appetite for spot ETFs in the United States and further strengthens the bears’ argument of a lack of investor demand.

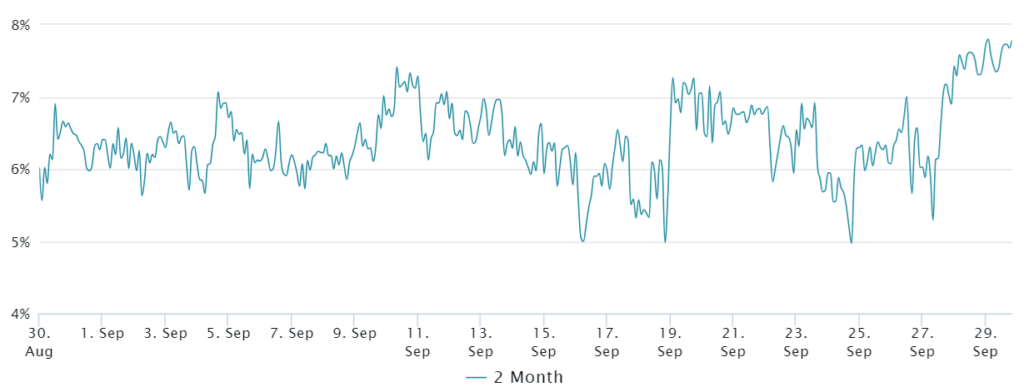

Investors’ lack of conviction is also evident in the Bitcoin futures markets, even in monthly contracts typically preferred by whales and institutional investors due to their absence of fluctuating funding rates. In neutral markets, these derivative contracts tend to trade at a 5% to 10% annualized premium to account for their longer settlement periods.

Bitcoin 2-month futures annualized premium. Source: Laevitas.ch

Data shows that the Bitcoin futures premium stabilized at 6% despite the rally toward $66,000 on Sept. 29. These savvy derivatives traders maintained their neutral stance, displaying reluctance driven by fear of missing out, but at the same time may have given bears exactly what they needed—a signal of a lack of conviction.